Why Saving Money Is Important: The Complete Guide to Saving Money: Practical Tips for a Strong Financial Future

Saving money is one of the most important habits a person can develop. It creates security, reduces stress, and gives you the freedom to make better life decisions. Many people believe saving is only possible when income is high, but the truth is that saving depends more on habits than on income level. Even small, regular savings can grow into a strong financial foundation over time.

This article explains practical and realistic ways to save money, build discipline, and create a secure future.

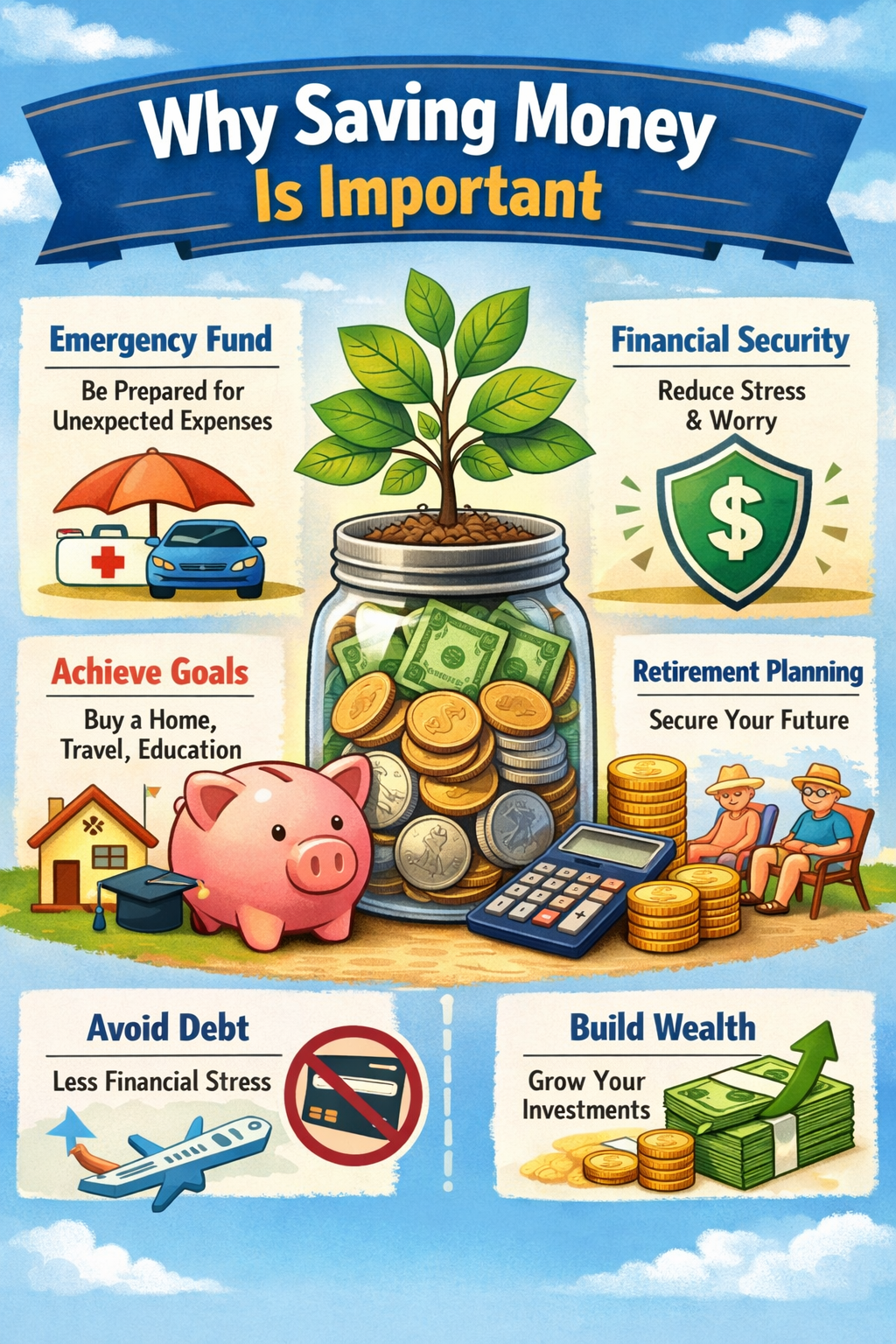

Why Saving Money Is Important

Saving money is not just about storing cash. It is about preparing for the future and protecting yourself from financial difficulties.

1. Financial Security

Life is unpredictable. Emergencies like medical expenses, job loss, or sudden repairs can happen at any time. Savings act as a safety net.

2. Freedom of Choice

When you have savings, you can make decisions without fear. You can change jobs, start a business, or take a break if needed.

3. Reduced Stress

Money problems are one of the biggest causes of stress. Having savings gives peace of mind.

4. Future Planning

Savings help you achieve long-term goals like buying a house, starting a business, or retiring comfortably.

Step 1: Set Clear Financial Goals

Saving without a goal often leads to failure. Goals give direction and motivation.

Types of Financial Goals

Short-term goals (0–1 year):

- Emergency fund

- Paying off small debts

- Saving for a gadget or trip

Medium-term goals (1–5 years):

- Buying a vehicle

- Starting a business

- Education expenses

Long-term goals (5+ years):

- Buying a house

- Retirement savings

- Children’s education

How to Set a Good Goal

Use the SMART method:

- Specific

- Measurable

- Achievable

- Relevant

- Time-bound

Example:

“Save ₹50,000 in 10 months by saving ₹5,000 each month.”

Step 2: Understand Your Income and Expenses

You cannot save money if you do not know where it goes.

Track Your Spending

For one month, write down:

- Every purchase

- Every bill

- Every online payment

You will start to notice patterns in your spending.

Divide Expenses into Categories

Needs:

- Rent

- Groceries

- Utilities

- Transportation

Wants:

- Eating out

- Entertainment

- Shopping

- Subscriptions

This separation helps you see where you can reduce spending.

Step 3: Create a Simple Budget

A budget is a plan for your money. It tells you how much to spend and how much to save.

The 50-30-20 Rule

- 50% for needs

- 30% for wants

- 20% for savings

If 20% feels difficult, start with 5–10%. The key is to begin.

Example Budget

Monthly income: ₹30,000

- Needs: ₹15,000

- Wants: ₹9,000

- Savings: ₹6,000

Even saving ₹3,000 per month will become ₹36,000 in a year.

Step 4: Cut Unnecessary Expenses

Small expenses often go unnoticed but add up quickly.

Common Money Leaks

- Daily snacks or coffee

- Unused subscriptions

- Impulse shopping

- Frequent food delivery

Simple Ways to Reduce Spending

- Cook more meals at home.

- Buy in bulk for essentials.

- Use public transport when possible.

- Repair items instead of replacing them.

The 30-Day Rule

Before buying a non-essential item:

- Wait 30 days.

- If you still need it, then buy it.

This prevents emotional spending.

Step 5: Pay Yourself First

Most people spend first and save whatever is left. This usually results in no savings.

Instead:

- Save first.

- Spend what remains.

How to Do It

- Set automatic transfers to a savings account.

- Treat savings like a monthly bill.

Even small amounts build strong habits.

Step 6: Build an Emergency Fund

An emergency fund is your financial protection.

How Much to Save

Aim for:

- 3–6 months of living expenses

Example:

If your monthly expenses are ₹15,000:

- Emergency fund goal = ₹45,000 to ₹90,000

How to Build It

- Save a fixed amount every month.

- Use bonuses or extra income to grow it faster.

Only use this fund for real emergencies.

Step 7: Avoid and Reduce Debt

Debt reduces your ability to save.

Tips to Manage Debt

- Pay high-interest debts first.

- Avoid unnecessary loans.

- Use credit cards carefully.

- Never spend more than you can repay.

Snowball Method

- Pay off the smallest debt first.

- Move to the next one.

- Continue until all debts are cleared.

This builds motivation.

Step 8: Increase Your Income

Sometimes saving more requires earning more.

Ways to Earn Extra Money

- Freelancing online

- Selling handmade or used items

- Tutoring students

- Starting a small online store

- Doing part-time work

Even a small extra income can boost savings.

Step 9: Develop Smart Shopping Habits

Smart spending helps you save without feeling deprived.

Practical Shopping Tips

- Make a shopping list.

- Compare prices before buying.

- Look for discounts and sales.

- Avoid shopping when bored or emotional.

Buy Quality, Not Quantity

Cheap products often wear out quickly.

Quality items last longer and save money in the long run.

Step 10: Save Windfall Money

Unexpected money should not become unexpected spending.

Examples:

- Bonuses

- Gifts

- Tax refunds

- Prize money

Save at least 50–80% of such income.

Step 11: Start Investing

Saving protects money.

Investing helps it grow.

Once you have:

- An emergency fund

- No high-interest debt

You can begin investing.

Basic Investment Options

- Fixed deposits

- Recurring deposits

- Mutual funds

- Retirement plans

Start small and increase gradually.

Step 12: Stay Consistent and Patient

Saving money is not a one-time action. It is a lifestyle.

Ways to Stay Motivated

- Track your savings monthly.

- Celebrate small achievements.

- Visualize your financial goals.

- Avoid comparing yourself to others.

Consistency matters more than the amount.

Saving ₹50 daily:

- ₹1,500 per month

- ₹18,000 per year

Small steps create big results.

Common Mistakes to Avoid

- Not tracking expenses

- Saving only what is left

- Ignoring small daily spending

- Using savings for non-emergencies

- Depending only on one income source

Avoiding these mistakes improves your financial health.

Daily Habits That Help You Save

- Carry a water bottle instead of buying drinks.

- Turn off unused lights and appliances.

- Cook meals at home.

- Plan weekly expenses.

- Walk short distances instead of using vehicles.

These habits seem small but create large savings over time.

The Power of Consistency

Saving is not about perfection.

It is about discipline and patience.

If you save regularly:

- You gain financial confidence.

- You reduce stress.

- You build a secure future.

Your income may change, but strong saving habits will always protect you.

Final Thoughts

Anyone can save money with the right mindset and habits. You do not need a large salary to begin. What matters most is consistency, discipline, and clear financial goals.

Start small.

Stay consistent.

Build strong financial habits.

Your future self will thank you for the decisions you make today.